E.SUN established a standardized carbon inventory mechanism to manage carbon emission data in accordance with the PCAF Standard through its Financed Carbon Emissions Inventory Management System. With this system, we have increased the automation rate, improved efficiency, and reduced operational risks. Technology assists in the generation of financed carbon emission information and target management, enabling us to respond to potential risks and opportunities in real-time.

The physical risks of climate change pose a significant challenge to the operational resilience of banks. In addition to the potential disruption of business operations, which may impact customer service and revenue, the depreciation of credit collateral value is also a major concern. To effectively manage climate-related physical risks, E.SUN has established an internal physical risk database that integrates with its business systems to provide decision-making information. We will continue to expand our collection of climate-related risk data in order to enhance the ability of frontline staff to identify physical risks.

Since 2022, E.SUN has been implementing the LEAP methodology and has been at the forefront of integrating the Task Force on Climate-related Financial Disclosures (TCFD) and the Task Force on Nature-related Financial Disclosures (TNFD) frameworks by publishing its "Climate and Environmental Report." This report focuses on both climate change and biodiversity, with "Nature Positive" as a key goal. The report has received recognition from the TNFD secretariat and has been shared on social media, making it a featured case study in the TNFD's Guidance for Financial Institutions. E.SUN further strengthens its commitment by being among the first globally to join TNFD Early Adopters, taking concrete action to care for this beautiful land.

| 2020 | 2021 | 2022 | 2023 | |

|---|---|---|---|---|

| Scope 1 | 2,399 | 1,858 | 1,844 | 2,161 |

| Scope 2 | 22,299 | 22,105 | 20,294 | 17,959 |

| Scope 3: Financed Emissions | 4,710,269 | 3,672,612 | 4,945,550 | 5,355,042 |

| Scope 3: Others | 53,713 | 49,181 | 56,015 | 46,436 |

| Total (Tons) | 4,788,679 | 3,745,755 | 5,023,703 | 5,421,598 |

Note: Scope 2 emission is calculated using market-based methods.

| 2020 | 2021 | 2022 | 2023 | |

|---|---|---|---|---|

| Financed Emissions( t-CO2e) | 4,710,269 | 3,672,612 | 4,945,550 | 5,355,042 |

| Carbon Footprint (t-CO2e/$M) | 2.44 | 1.73 | 2.10 | 2.14 |

| Weighted Average Carbon Intensity (t-CO2e/$M) | - | 6.23 | 4.77 | 5.09 |

| Inventory Coverage (%) | 73.69% | 75.27% | 76.53% | 77.62% |

Note 1: Emissions from investment and financing activities for 2023 have been estimated based on the changes in our total assets reported in our financial statements

Note 2: Carbon Footprint = GHG emissions from investment and financing companies / inventoried balance of investment and financing companies

Note 3: Inventory Coverage = inventoried balance of investment and financing companies / sum of FVPL, FVOCI, AC, loans, and discounted items

Note 4: Inventory coverage for 2023 using PCAF methodology is 100%

Note 5: Currency shown in $USD, calculated using USD/TWD exchange rate of 12/31/2023

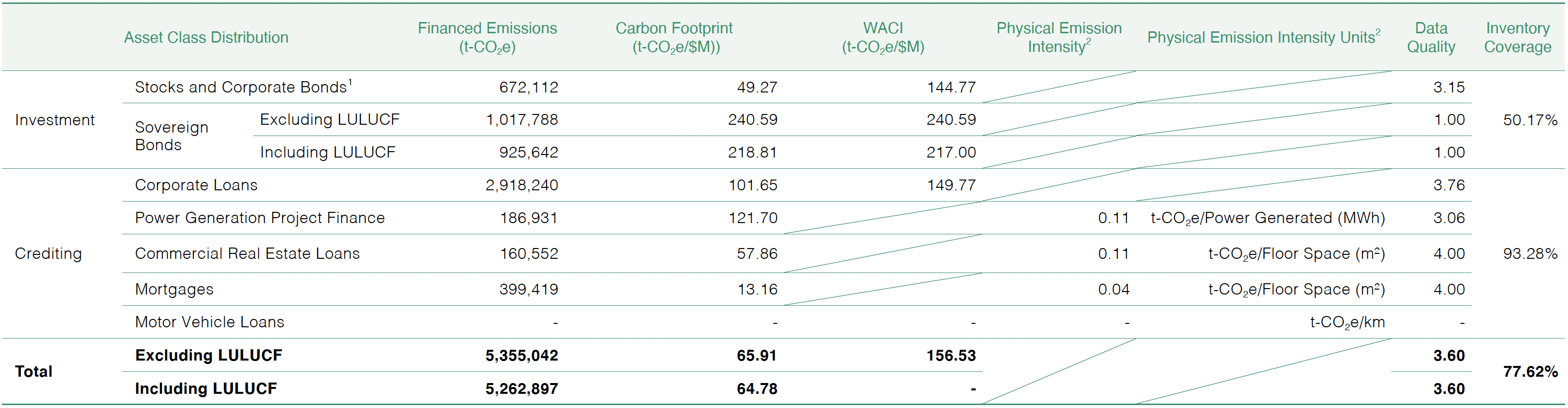

E.SUN analyzes the GHG emissions of its investment and financing assets based on asset types, industry, and regions. We have set different decarbonization goals for different asset types according to SBT targets and plan control mechanisms for high-carbon industries. We also engage with customers and encourage staff to increase interaction with low-carbon companies or investment targets. We hope to leverage our financial influence to help achieve net-zero emissions.

| Geographical Distribution | Financed Emissions (t-CO2e) |

Carbon Footprint (t-CO2e/$M) |

WACI (t-CO2e/$M) |

| Taiwan | 3,140,494 | 1.73 | 5.31 |

| N. America & Europe | 655,654 | 2.13 | 1.75 |

| Other Asia | 558,060 | 3.69 | 5.10 |

| Others | 555,881 | 3.72 | 9.07 |

| Hong Kong | 396,865 | 6.48 | 10.36 |

| China | 48,089 | 4.39 | 4.21 |

| Total | 5,355,042 | 2.14 | 5.09 |

| Industry distribution | Financed Emissions (t-CO2e) |

Carbon Footprint (t-CO2e/$M) |

WACI (t-CO2e/$M) |

| Manufacturing | 1,051,005 | 5.32 | 5.20 |

| Electricity and Utilities | 613,580 | 9.14 | 57.45 |

| Fossil Fuels and Chemical | 463,116 | 8.06 | 14.78 |

| Transportation | 540,763 | 9.22 | 14.95 |

| Electronics | 327,248 | 2.65 | 3.46 |

| Others | 424,580 | 1.49 | 2.99 |

| Cement and Glass | 197,443 | 36.43 | 122.02 |

| Metals and Mining | 145,813 | 11.70 | 12.70 |

| Wholesale and Retail Trade | 113,156 | 0.65 | 0.43 |

| Finance | 61,131 | 0.13 | 0.31 |

| Total | 3,937,835 | 2.74 | 4.82 |

For more details on Net Zero actions, please refer to the latest Sustainability Report.